Credit Strategies Indicators Roll Red In April

Destra Capital

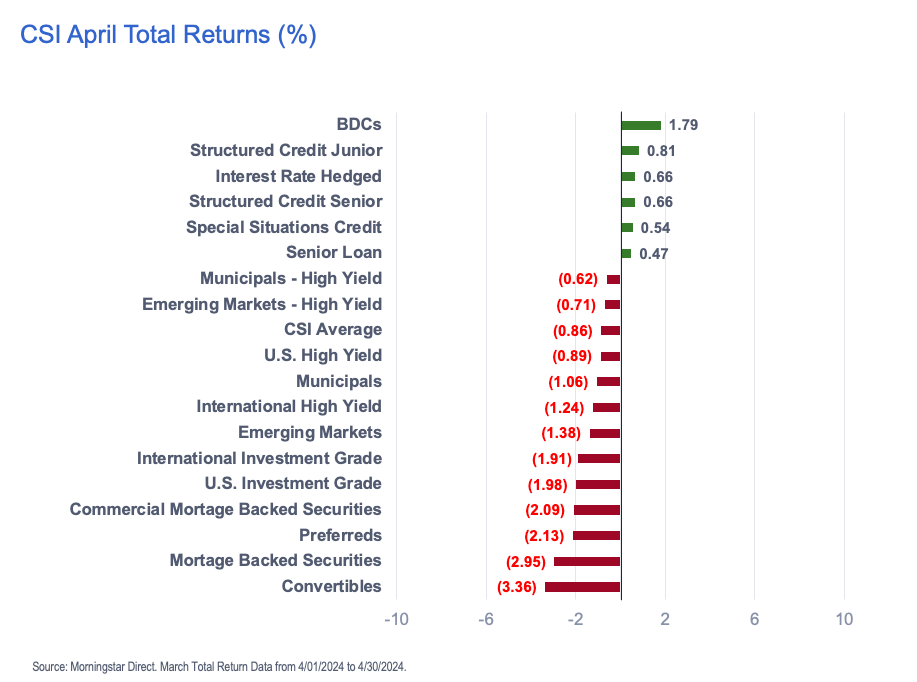

April saw the Destra Credit Strategies Indicator (“CSI”) deliver an overall negative result of -0.86% on average with 12 of 18 sub-strategies declining on a total return basis for the month. This was a far cry from March, when the CSI was up a positive +1.33% on average and 17 of 18 categories were green!

Macro Meltdown

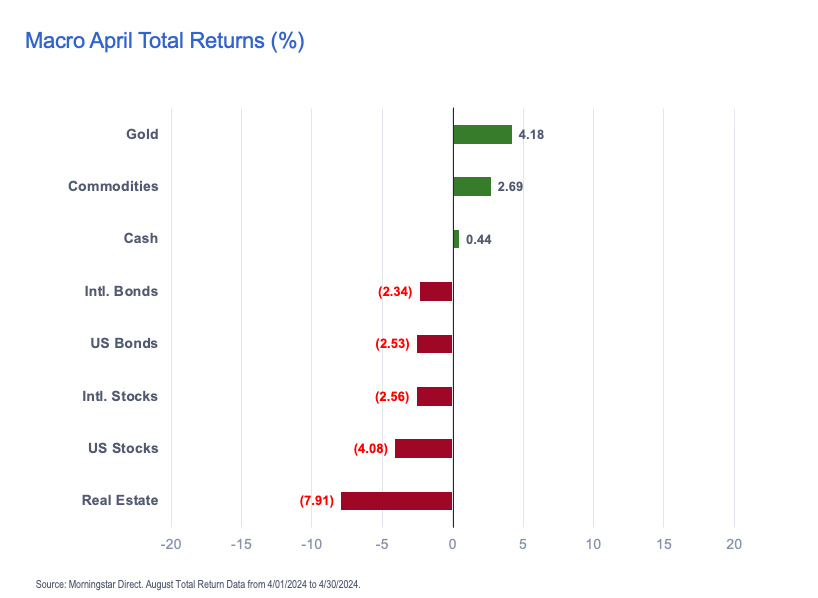

But credit markets were not alone in the pullback in April. Many of the traditional macro asset class benchmarks withered as rates stayed higher for longer, Russia continued to press their assault on Ukraine and the Middle East nearly boiled over.

What’s In a Name?

From time to time, Destra reviews the categories that we track in the CSI and revisit the constituents that make up each of the sub-categories and their strategy names and identities. This month, we have made a change to the identify and classification of one or our sub-strategies : the former “Event-Driven Credit” category will now be called the “Special Situations Credit” category. While there is no change to the underlying constituent funds that feed into the indicator, the name change reflects more current industry language and terminology around stressed, distressed and opportunistic credit investing. From a performance standpoint, the results from this sub-set of credit investing continue to move along nicely….the newly rechristened Special Situations strategy was up +0.54% for the month, bringing it to a +3.88% year to date through the end of April. In fact, it was one of only 6 sub-strategies in the CSI to make it into the green for the month.

It's An Old Fashioned, What Could Go Wrong…

That is still one of my favorite all time movie lines….extra points for anyone who can guess the movie! Looking at good old fashioned US High Yield or Senior Loan investing, there did not seem like there was much that the market thought could go wrong in April. John Authers of Bloomberg noted this past month, “…as far as the credit market is concerned, there’s nothing to worry about.” And looking at credit spreads, that certainly seemed true.

But while Senior Loans put up positive results in April with a +0.47%, their kissing cousins in High Yield came under pressure, down -0.89%. Spread are tight, but perhaps the patience of the market for leveraged companies is waning as the Fed keeps kicking the can down the road.

Long and Wrong

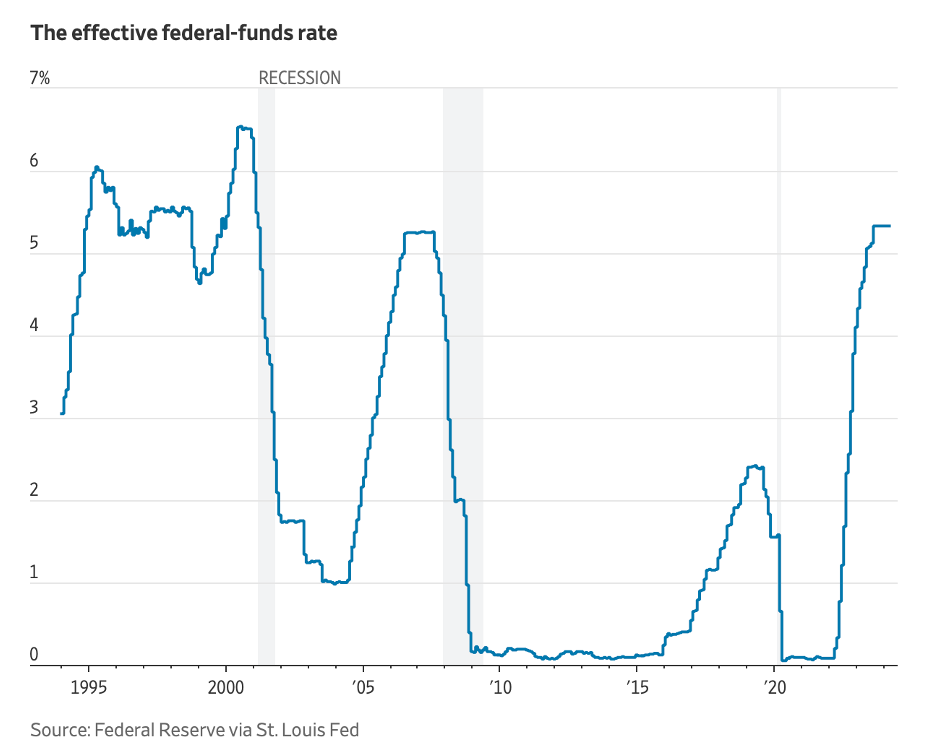

And speaking of the Fed, Chairman Powell and his cohorts spent much of April suggesting that the “data” did not give them much encouragement that rates would be coming down anytime soon.

This led to negative outcomes for CSI strategies that are typically seen as longer in duration or more spread sensitive such as Municipals -1.06%, Preferreds -2.13%, Investment Grade -1.98% and International Investment Grade -1.91% to name a few.

Real Pain In Real Estate

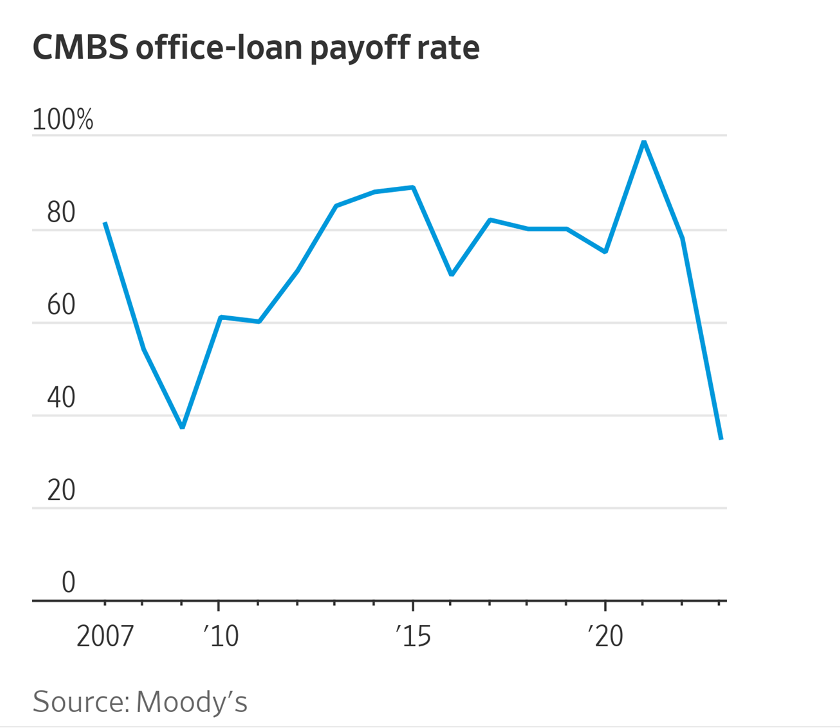

The credit strategies that are associated with real estate, such as Mortgage Backed Securities and CMBS, were some of the worst performers for the month, down -2.95% and -2.09% respectively. And the story line seems to just get bleaker there as well, with the Wall Street Journal commenting that, “…defaults are reaching historic levels in the office market, as a growing number of owners capitulate to persistently high interest rates and weak demand.”

Power To The Privates!!

As this edition of Credit Events went to print, the news broke that Pacific Gas & Electric (“PG&E”) was in talks to sell a huge block of its infrastructure to KKR in a bid to raise capital. Let’s not unpack why PG&E needs to sell off the choice bits of its infrastructure to a private credit shop like KKR just yet, but suffice to say, as a society we are going to find out that tilting at windmills (and solar panels) is not going to be as easy peasy as the greenest of us would have the rest of us believe!

Just this week, Apollo’s Chief Economist, Torsten Sløk commented that the vast amount of employment in the US economy came from private firms, not public ones.

One of the ways that credit investors can get exposure to private credit is through the origination services of BDCs, which had yet again another stellar April, up +1.79%, delivering the best performance in the CSI for the month.

Credit Events Webinar

As April came to a close, we held a special Destra Credit Events webinar with Adam Phillips who Heads the BlueBay Developed Markets Special Situations Desk at RBC Global Asset Management in London. Adam walked the webinar participants through the opportunity to consider stressed and distressed debt in a portfolio and where his colleagues were finding value today. If you are interested in learning more about this unique and alternative form of credit investing, please visit the link HERE to listen to a replay of the webinar.

Thanks and we will be back in early June to recap May across the credit investing landscape.