Summer Blockbusters!

Destra Capital

June 4, 2024Memorial Day is behind us now and it is time for the Summer Blockbusters. So with a nod to great movie quotes of the past, here is your May Credit Events newsletter!

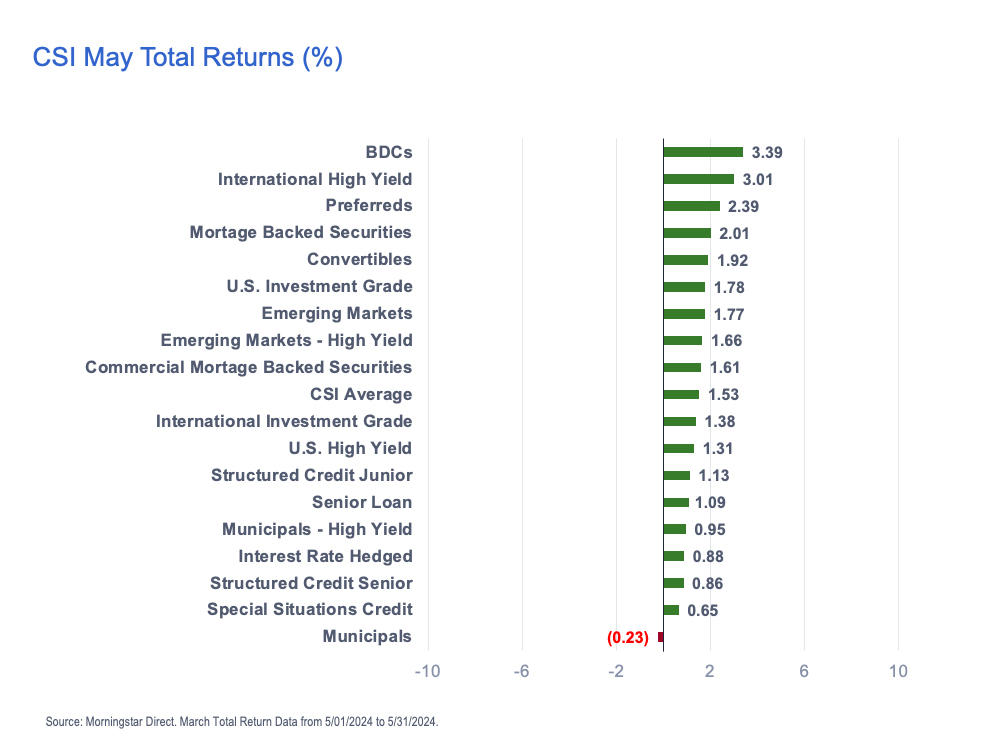

Everything’s So Green!1

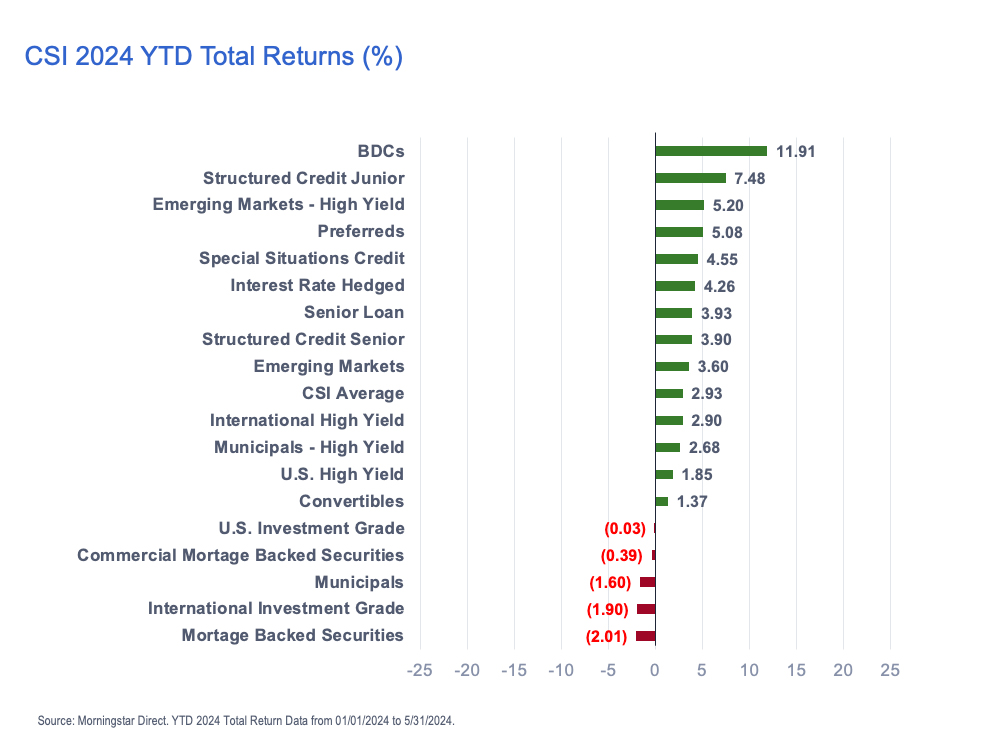

Destra’s Credit Strategies Indicator (“CSI”) was nearly all green in May, with 17 of 18 categories recording positive total returns for the month. This brought the year to date numbers up to 13 positive and only 5 negative for the first five months of the year.

On average, May saw a +1.53% for the CSI, with BDCs the big winner, up +3.39% and only Muncipals in negative territory, for the month, down -0.23%.

Year to date, the BDC credit strategy is way out in front, with a positive total return of +11.91%, followed by the Structured Credit Junior Tranche strategy +7.48% and Emerging Markets – High Yield, up +5.20%. The bottom three strategies were Municipals, down -1.60%, International Investment Grade, down -1.90% and Mortgage Backed Securities, down -2.01%. The average for the CSI across all 18 categories year to date is a positive +2.93%.

You Can’t Handle (Realize) The Truth!2

Preferreds are mostly issued by banks and insurance companies and therefore have a huge bias toward the health of financials. The Spring of 2023 saw a legit banking scare with several big US regionals and the storied Swiss bank, Credit Suisse, all going down. This year, there was a bit of a mini scare a few months ago when New York Community Bank hit the skids, but overall banks have held up in 2024 and investors have generally agreed with the Destra CSI Preferred category posting a positive +5.08% return year to date.

But there are still concerns about the underlying exposures of many banks to real estate and to their investment portfolios.

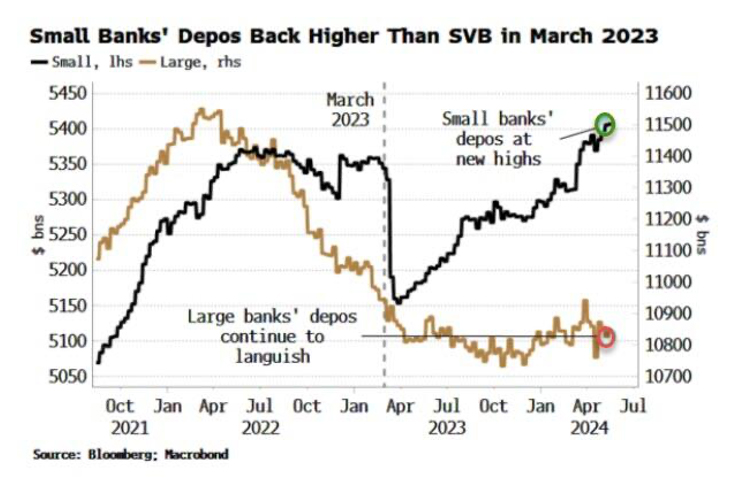

Zuzu’s Petals, There They Are!3

And it is not just the big banks that seem to be defying the concerns of investors, small banks are getting healthy too. According to ZeroHedge,….

“The Fed can rejoice in its success in preventing a wider banking crisis after Silicon Valley Bank’s failure. Deposits in small banks have now fully recovered. The Bank Term Funding Program, and a blanket deposit-guarantee for SVB and Signature Bank - which went down soon after Silicon - healed confidence in the sector.”

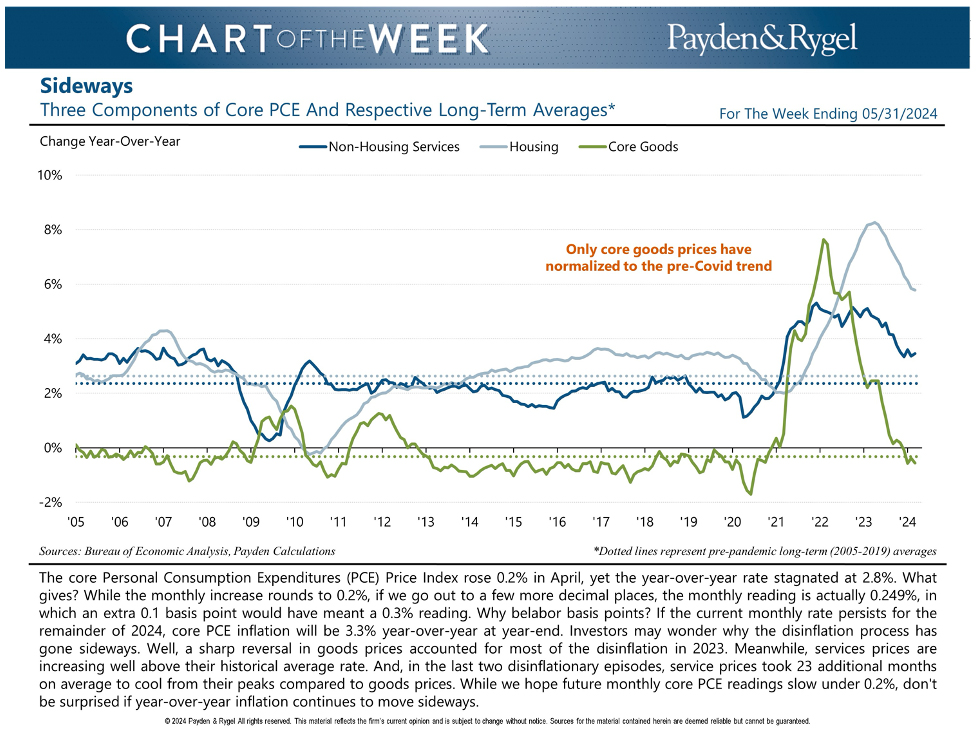

I Am Not Drinking Merlot!4

While inflation has slowed a bit, it is not cool by any stretch of the imagination. The economics team over at Payden & Rygel had a great chart this week that breaks apart the principal components of the PCE and shows that Housing and Services are stubbornly high.

Perhaps the persistence of inflation is keeping pressure on investment grade strategies because both the US (-0.03%) and International Investment Grade (-1.90%) credit strategies are negative, year to date in the CSI.

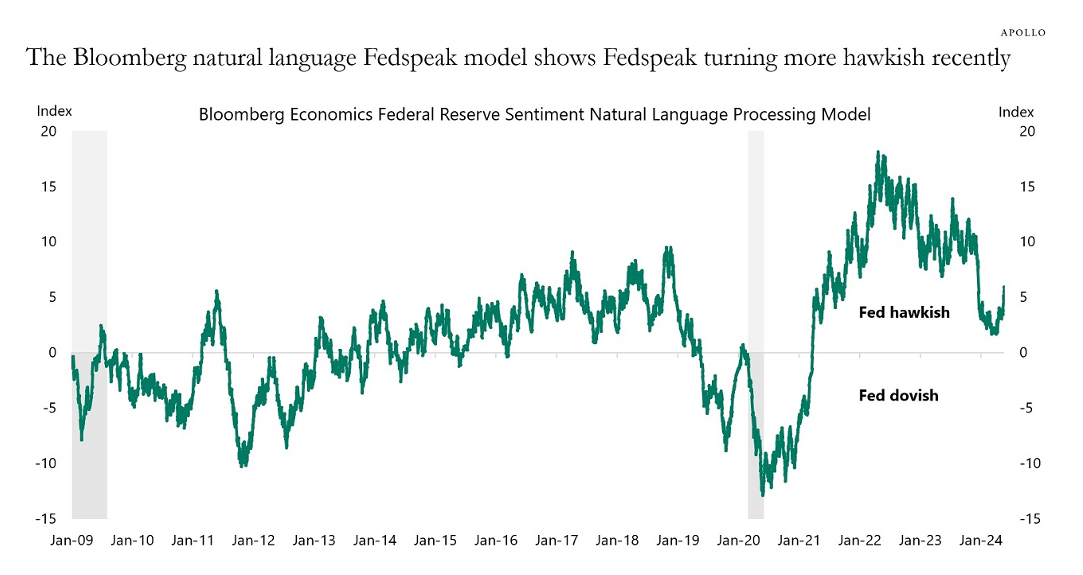

Cut the Fed Funds Rate, Please, Hal.5

All things “artificial intelligence” seems to be hot right now. Even Bloomberg is getting in on the act, according to Torsten Sløk, the Chief Economist over at Apollo. He notes….

“The Bloomberg natural language processing model analyzes Fed speeches and currently shows FOMC members moving toward a tightening bias, see chart below.Note how the model never predicted rate cuts in 2024. Instead, Fed sentiment has simply been less hawkish in 2024 than in 2022 and 2023.The bottom line is that this Fed sentiment model using data back to 2009 shows that Fed communication continues to favor Fed hikes rather than Fed cuts.”

Source: Bloomberg, Apollo Chief Economist. Note: Fedspeak: NLP model of Fed sentiment. The index is underpinned by an NLP algorithm trained on Bloomberg News headlines, covering about 6,200 speaking engagements by Fed officials since 2009. A reading below zero implies rate cuts, while above zero indicates a tightening basis.

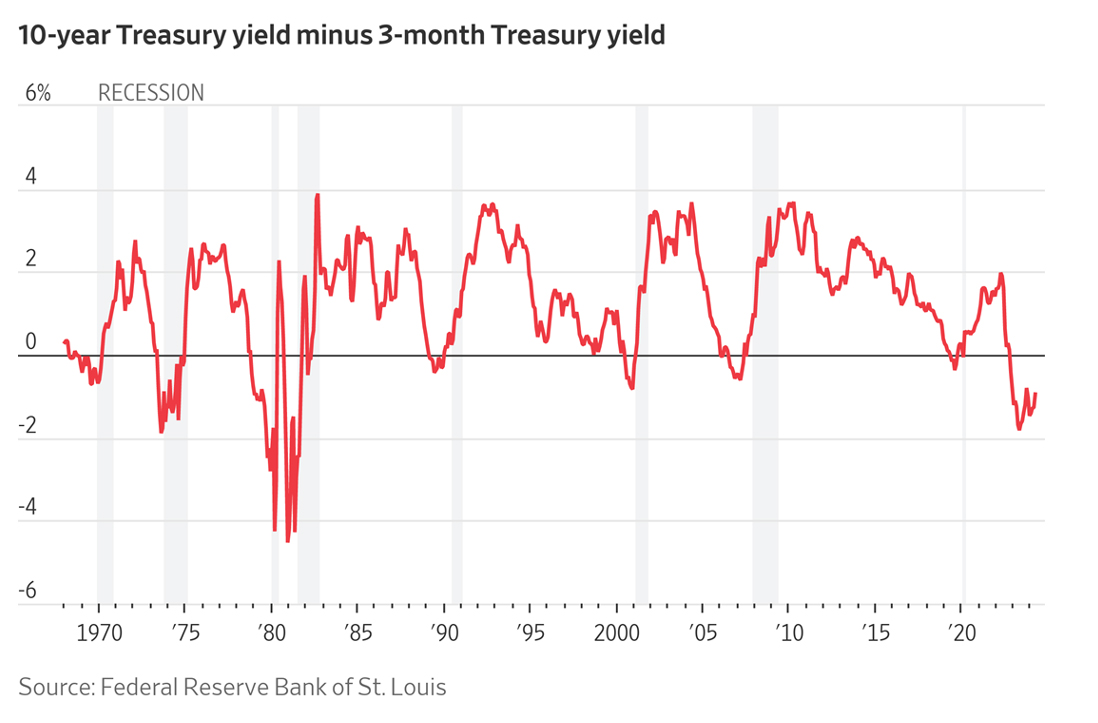

You Were In A 4G, Inverted Dive With A Mig-28? 6

The Wall Street Journal commented last week that the supposed bellwether signal for recession, an inverted yield curve, was at risk of losing its credibility.

“An inverted yield curve, in which yields on short-term Treasurys exceed those of longer-term government debt, has long been taken as a nearly surefire signal that an economic pullback looms. But the yield curve now has been inverted for a record stretch with no signs of a major slowdown.”

Who knows if any of the movies slated to come out this summer will approach the blockbuster status of the ones we quoted here, but we will keep an eye out for them and report back in future editions of Credit Events to let you know how the summer pans out at both the theater and in the credit markets.

- 1) History of the World, Part I.

- 2) A Few Good Men

- 3) It’s A Wonderful Life

- 4) Sideways

- 5) 2001 A Space Odessey

- 6) Top Gun (the original)